DBOE is back with another academic session to continue guiding you in understanding options trading at a much deeper level. DBOE has previously discussed how options are priced. Two important concepts are mentioned: intrinsic value and extrinsic value. Today, DBOE will dive deeper into understanding those two concepts.

Recalling Options Premium:

An option price, also known as an option premium, is the price a buyer pays to purchase an options contract. The premium consists of two main components: intrinsic value and extrinsic value.

Unveiling the Core: Decoding Option Intrinsic Value

In an incredibly simplified definition, the intrinsic value of an option is the difference between the strike price and the underlying asset value if the contract is exercised today. However, the formula is the same but different for call and put options.

- Call option: Underlying Asset Price – Strike Price

- Put option: Strike Price – Underlying Asset Price

For example, to calculate the intrinsic value of a call option contract on DBOE, you would use the underlying asset price and subtract the minimum price range. On August 9th, 2024, SOL/USD price is $157.40. If I execute this call option with a price range between 150-165, the intrinsic value would equal:

$157.40 – $150 = $7.4

However, this contract would have no intrinsic value if you select the option with a price range of between $160 and $175. Thus, for a call option to have intrinsic value, the strike price has to be lower than the asset price. The opposite is applied to a put option. If this factor is not satisfied, an option has no intrinsic value.

Beyond the Surface: Exploring Option Extrinsic Value

Extrinsic Value is a combination of implied volatility and time value. Here is the formula for extrinsic value:

Options Premium – Intrinsic value = Extrinsic Value, where Extrinsic Value = Time Value + Implied Volatility

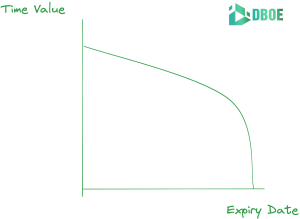

Firstly, time is vital in options trading, like many other assets. So, how does the time value change? As the contract is closer to its expiry date, the time value decreases; the graph below will explain this:

Let’s use DBOE as an example. For context, 1-week is the only expiry date, usually at 8 AM UTC, 3 PM ICT, or 4 PM SGT every Friday. Suppose you buy two contracts, one on Monday and one on Wednesday. The Monday contract will have a higher extrinsic value than the Wednesday contract, keeping the implied volatility the same. Why? Because the contract will have longer to profit from a favorable move in the underlying asset.

Secondly, implied volatility talks about the expected movement of the underlying asset price

This factor is directly related to the asset’s demand and supply and the market’s expectations. Calculating the implied volatility is difficult since one must use the Black-Scholes Model. While there are other methods to calculate and approximate the implied volatility, there isn’t a simple way to find it because this concept allows investors to predict the future movement of the derivative.

Conclusion:

Ultimately, investors should realize that understanding both intrinsic and extrinsic value is vital to understanding the options premium in depth. Those two factors determine the movement of the option’s premium, and by understanding them, investors will have a more timely and informed decision to invest. Now, join our growing DBOE community to experience our multifaceted ecosystem to trade and learn more about options for future growth!

——————————————————————————–

At DBOE, we provide comprehensive resources and support to help you navigate the complexities of options trading. We aim to make options trading more secure and accessible.

Start your options trading journey with DBOE today at: Website or Mobile app.

Disclaimer: The information in this article is not intended as investment advice. Cryptocurrency investment activities are not legally recognized or protected in some countries. Cryptocurrencies always involve financial risks.